Structuring Your Property Investments (Part 2)

Getting your loan structures right from the start will eliminate costly problems down the track, writes Andrew Pribil

Following last month’s blog on structuring property investments, which looked at the common issue of an inefficient split between tax deductible and non-tax deductible debt, I have received various questions from property investors looking at the best way to build their portfolios. This month I’ll expand on the topic of property investing by taking you through the most effective way to commence growing your asset base, highlighting some of the key considerations that can save investors thousands of dollars by getting the loan structure right from the beginning.

Why do we worry about loan structures?

The emphasis last month was on raising client awareness around the need to have an efficient split between tax deductible and non-tax deductible debt (ensuring the debt on the home loan isn’t disproportionately large compared with investment property loans). Whilst tax implications more broadly are one of the main considerations, particularly for new market entrants, there are several other issues that are often overlooked by lenders and borrowers who don’t understand how loan structures can impact future financial objectives.

Tax implications – Naturally, property investors want to maximise the benefits that can be obtained through negative gearing. This is a scenario where the interest paid on an investment loan is greater than the income generated from the asset, with the difference effectively being deducted from total taxable income at the end of the financial year. As well as the issues raised in last month’s blog around the split between the amount owing on the borrower’s principal place of residence and the total debt on investment property loans, borrowers also need to ensure they have timely access to the correct type of capital whenever they identify an investment opportunity.

I will expand on this when discussing the ideal loan structure, but borrowers need to remain conscious of how they use available equity to fund the deposit for any investment property purchases. The Australian Taxation Office (ATO) uses a purpose test to gauge whether debt is classified as an investment loan (tax deductible) or personal (non-tax deductible). As a result, investors must ensure they are not accessing redraw on their home loan or other capital to pay the deposit for an investment property purchase (please see ‘The Ideal Structure’ below).

Reduced asset protection – This is a common issue for any lending being done through a discretionary trust, where one of the main objectives is asset protection. A discretionary trust has two key benefits – the first being tax flexibility, as the trustee can distribute both income and capital at their discretion, and the other being asset protection. The problem with these scenarios arises when the deposit loan for the investment property (as mentioned above) is written in the name of the individual(s), with the money on-lent to the trust, rather than the debt being in the name of the trustee. Similarly, I often see personal assets cross collateralised with the property purchased by the trustee. These are regular structural issues we come across, with the potential implications being severe. If a trustee were to go into bankruptcy, or a client takes action against a company involved in the transaction, personal assets often need to be sold, as these structures don’t allow for the appropriate separation of personal and trustee/company assets. There is a way to structure these scenarios to avoid such problems, so please ensure you engage a knowledgeable broker to manage these transactions.

Cross collateralisation – Whilst there are varying viewpoints on whether cross collateralisation should be used when structuring client loans, I definitely lean to the side of avoiding it if at all possible. Banks will always want to hold as much security as possible to ensure sufficient protection, but the borrower will also want to avoid being forced to sell personal assets they have tied to investment loans (or even business loans) if they face hardship. Take Michael & Tina as an example, who have used their home to help securitise the purchase of their investment property and avoid Lenders Mortgage Insurance (LMI). Their $800,000 home has only $200,000 owing, so this equity has been added as security to fund their $400,000 investment property purchase. After including costs of around $40,000, this takes the total loan to $440,000, being secured by the investment property itself ($400,000) & the $600,000 of equity in the principal place of residence.

Two years after purchasing the investment property, Michael & Tina run into financial trouble and can no longer pay their investment loan. Given both homes are being used to secure the investment property the bank can force the clients to sell both properties. As Michael & Tina have borrowed the full amount plus costs for the investment property, are under financial duress and face a fire-sale (immediate sale of the property forced by the bank), it is unlikely they will be able to cover the full amount by selling only the investment property. To understand how lending is ideally structured considering the clients’ tax position, asset protection and avoiding cross collateralisation where possible, see the next section on ‘The ideal structure to build your investment property portfolio’.

The ideal structure to build your investment property portfolio

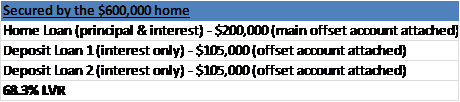

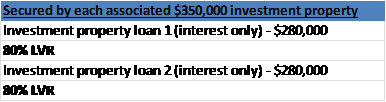

To explain the ideal structure of a lending portfolio that enables the purchase of multiple investment properties, we will use another example. Ryan & Ashlea plan to build an extensive property portfolio. With only $200,000 owing on their home worth $600,000 ($400,000 in equity), they are in a position to commence purchasing their investment properties. What we want to do from here is maximise the tax deductible debt as a percentage of non-tax deductible debt, whilst separating these loans for account keeping purposes and ensuring quick and easy access to capital. Another aim is to minimise costs, so the loan to value ratio (LVR) will need to be kept at 80% or below to avoid LMI.

Step 1 – First of all, we need access to capital to pay the deposit of 20% plus costs. Whilst Ryan & Ashlea are keen to purchase an investment property now, they are looking to build a property portfolio, so we will provide them with two interest only loans that will fund the deposit for each investment property worth $350,000 plus costs of ~$35,000 (stamp duty, legal fees, bank fees, etc.) relating to each purchase. As a result, two deposit loans of $105,000 each (20% deposit plus $35,000 in costs) will be established, using equity in the home as security. The deposit loans are kept separate from the home loan for account keeping purposes and to ensure the purpose of funds is clear so full tax benefits can be claimed.

Step 2 – Set up two more offset accounts attached to each deposit loan, which are completely separate from the home loan. All disbursed funds from each deposit loan will enter the associated offset accounts upon draw down. As the loans are set as interest only and the offset balances perfectly match the loan balances, there will be no impact to the customers’ cash flow whilst searching for an investment property. For those unaware of how an offset account operates, please see information in our Home Buyers’ Guide.

Step 3 – Ryan & Ashlea are now ready to purchase their first investment property, drawing down the loan into the offset account and accessing the first $105,000 to pay for the deposit and associated costs. All rental income for this property will enter the offset account, where interest payments will also be deducted.

Step 4 – Find the second investment property and repeat step three, accessing the other $105,000 to purchase the next investment property. All rental income for this property will enter the offset account, where interest payments will also be deducted.

At the conclusion of the transaction, Ryan & Ashlea’s lending structure will look like this:

Any excess funds will be directed towards the home loan to expedite the pay down of the non-tax deductible debt, with the loans for investment purposes will remain interest only until the mortgage is fully paid down.

It is also important to note that we would ideally have each security aligned with the relevant loan(s). As a result, in a few years when the investment property values increase, the structure can be tidied up so each investment property is securing the associated deposit loan, and potentially being merged with the related investment loans.

As can be discerned from reading this information the process can seem slightly exhaustive, so please give me a call if you would like to start building your property portfolio or are unsure of whether your loans are presently structured correctly.

Choices today for a secure tomorrow.

Andrew

Previous Post

Previous Post